100% Focus on Your Recovery,

Chicago Auto Accident Lawyer

Chicago Auto Accident Lawyer

Our Team of Attorneys Are Committed to Maximizing the Value of Your Case

If you’ve been injured in a crash, understanding Illinois car accident insurance coverage is a critical first step toward protecting your rights. Our law firm has helped countless drivers across Chicago and throughout the state recover compensation after serious accidents. With years of experience dealing with every type of insurance company, we know how to handle delays, lowball offers, and denied claims. As a trusted Chicago auto accident lawyer team, we focus on helping you recover damages for medical expenses, repair costs, and other financial losses. Whether you’re dealing with your own insurance company or the other driver’s, we’re here to help.

Illinois is an at-fault state, which means the driver responsible for causing a crash is also responsible for paying for the resulting damage. After an auto accident, the at-fault driver’s insurance company is typically required to cover the other party’s medical bills, property damage, and related losses, up to the policy’s liability limits.

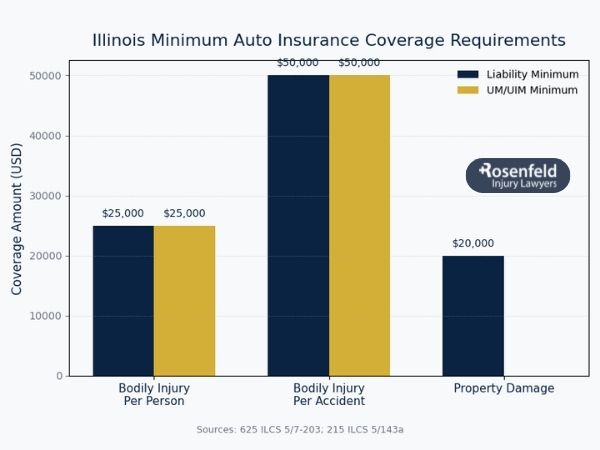

Under 625 ILCS 5/7-601, all drivers are required to carry minimum liability coverage. These auto accident laws in Chicago and Illinois ensure that victims can pursue compensation through the at-fault party’s liability insurance or, in some cases, their own insurance coverage.

Illinois law requires all drivers to carry liability insurance with minimum limits of $25,000 physical damage coverage per person, $50,000 per accident, and $20,000 property damage coverage. The law also mandates UM coverage with the same physical damage coverage limits to protect drivers hurt by an uninsured or hit-and-run driver. While these are the minimum limits, they often fall short in serious accidents. Medical expenses and repair costs can quickly exceed basic liability coverage. Many drivers choose to increase their liability limits or add underinsured motorist coverage, collision coverage, and medical payments coverage for added protection.

Driving without auto insurance in Illinois carries serious consequences. The Illinois Department of Transportation enforces penalties that may include fines ranging from $500 to $1,000 and suspension of your driver’s license and vehicle registration number. To reinstate driving privileges, offenders often must file an SR-22 form–proof of future financial responsibility–with their insurance provider for up to three years.

If an uninsured driver is involved in an auto accident, they may be personally responsible for covering financial losses, especially if they’re the at-fault party. Even if they’re not at fault, lacking insurance can limit the ability to recover damages from the other insurance company.

Car insurance coverage in Illinois depends on whether insurance is tied to the car or the driver, and this often varies by policy. In many cases, insurance follows the vehicle, meaning permissive use–when someone drives your car with your permission–is covered. However, coverage is governed by contractual policy language, and some insurance policies exclude certain drivers or limit coverage for household members. Driving for work may not be covered under personal auto insurance. Rental car exceptions also apply, depending on your policy and whether you have rental car insurance. Rideshare drivers often need special coverage, as personal policies exclude commercial use.

If you’re hit by an uninsured or underinsured driver in Illinois, your own uninsured or underinsured motorist coverage may help pay for your injuries. Under 215 ILCS 5/143a, Illinois law requires drivers to carry uninsured motorist coverage with at least the same bodily injury limits as the state’s minimum liability requirements. Underinsured motorist coverage applies when the at-fault driver’s liability limits aren’t enough to cover your medical expenses. In some cases, you can stack UM/UIM coverage if you have multiple vehicles insured. If coverage isn’t enough, filing a personal injury lawsuit may be necessary.

An umbrella policy can increase your liability protection after a serious auto accident, but it does not increase your Illinois collision coverage. Collision coverage pays for damage to your own vehicle, and its limits are set within your auto insurance policy. Umbrella policy car accident coverage is contractual and only extends liability limits, covering bodily injury or property damage when costs exceed your primary insurance coverage.

This excess coverage applies after your liability limits are exhausted and typically requires that you carry a certain amount of underlying coverage first. It won’t cover your own repair bills unless someone else is at fault.

Medical Payments coverage (MedPay) is optional insurance that helps cover medical expenses after an auto accident, no matter who was at fault. MedPay is contractual (policy-based), meaning coverage depends on the terms of your insurance policy, not state law. It can pay for ambulance rides, hospital visits, and follow-up care. If your health insurer covers the bills first, they may assert a lien against any future settlement. MedPay can reduce or satisfy that lien and is especially useful in covering early treatment costs while liability is still being sorted out with the other driver’s insurance agent.

Yes, hospitals and health insurers can reduce your car insurance claim through subrogation or medical liens. Under the Health Care Services Lien Act (770 ILCS 23/), medical providers can place a lien on any settlement or judgment you receive related to your accident. Health insurers may also assert a right to reimbursement through subrogation if they paid for your treatment. These liens reduce your net settlement because they must be paid out of any recovery. However, they can often be negotiated. A lawyer can help lower lien amounts and protect more of your compensation after an auto accident.

Illinois follows a modified comparative negligence rule under 735 ILCS 5/2-1116. If you’re found more than 50% at fault for an auto accident, you can’t recover any damages. If you’re 51% or less at fault, your compensation is reduced by your percentage of fault. Insurance companies often try to shift blame to minimize payouts. Even a slight increase in your assigned fault can significantly cut your settlement, so it’s essential to challenge unfair assessments.

Yes, Illinois auto insurance generally covers passengers injured in a crash, but the source of that coverage depends on who was at fault. A passenger can file a claim against the at-fault driver’s insurance agent, even if that driver was operating the passenger’s own vehicle. Some policies include household exclusions, which may limit coverage for relatives living in the same home.

Car insurance coverage for passenger injury can also come from uninsured or underinsured motorist policies if the responsible driver lacks enough coverage. Medical payments coverage may also apply, helping with immediate medical bills regardless of fault.

Auto insurance may cover rental cars in Illinois, but it depends on your policy. Rental car insurance is defined by individual policy contracts, so coverage varies. If you have rental reimbursement coverage, your insurance provider may pay for a rental while your own vehicle is being repaired after a covered accident.

If you’re driving a rental under permissive use, your own insurance might extend to that vehicle. Some credit cards also offer secondary rental coverage, but only if you decline the rental agency’s insurance. If another driver is at fault, their insurance company may be responsible for your rental costs.

Insurance coverage for Uber or Lyft accidents in Illinois depends on the driver’s status at the time of the crash. When the app is off, only the driver’s personal auto insurance applies. Once the app is on but no ride is in progress, Lyft insurance and Uber insurance requirements include limited liability coverage, typically $50,000 per person for bodily injury, $100,000 per accident, and $25,000 for property damage.

When a ride is accepted or in progress, both companies provide up to $1 million in liability insurance, along with uninsured/underinsured motorist coverage. This covers passengers, other drivers, and pedestrians injured in the crash. However, these policies only apply if the rideshare app is active. Drivers must still meet Illinois law for minimum insurance limits and may need rideshare-specific endorsements from their insurance provider.

Yes, Illinois liability insurance can cover bicycle and motorcycle crashes, depending on who was at fault. If a driver causes the crash, their liability insurance may pay for injuries or property damage. Cyclists may also use uninsured or underinsured motorist coverage from their own policy if the at-fault driver lacks coverage. Bicycle accident insurance claims often involve disputes over visibility, road position, or shared fault.

For motorcyclists, Illinois motorcycle accident insurance requirements include liability coverage, but many riders also carry collision coverage and medical payments. Because injuries are often severe, coverage limits and fault disputes play a significant role in the claim’s outcome. Working with a lawyer can help protect your rights and pursue full compensation.

Illinois truck accident cases often involve complex insurance issues due to the size of the vehicles and the severity of the injuries. Commercial trucking companies are required to carry higher liability limits under both Illinois law and federal regulations. Under 49 CFR 387.9, interstate carriers must have between $750,000 and $5 million in liability coverage, depending on the type of cargo.

These commercial truck insurance requirements are designed to cover serious bodily injury and property damage. In many cases, layered insurance structures apply, starting with a primary policy and followed by excess or umbrella coverage. Employer liability also plays a role, as trucking companies are often responsible for the negligent operation of vehicles operated by their employees. Claims can involve multiple parties, including the driver, trucking company, and insurance provider.

In Illinois, uninsured motorist coverage applies to hit-and-run accidents involving unidentified drivers. This coverage helps pay for bodily injury when the at-fault driver flees and cannot be identified. To use UM coverage, the crash must be reported to police promptly, and the insurance provider may require evidence that a hit-and-run occurred. Because proof can be challenging, working with a Chicago hit-and-run accident lawyer can help protect your claim and ensure proper documentation.

Under the Illinois car accident statute of limitations, victims typically have two years to file a personal injury lawsuit and five years for property damage. For uninsured or underinsured motorist claims, deadlines may be shorter and are often governed by your insurance policy’s terms. Breach of contract claims against your own insurance company, such as denial of coverage, generally must be filed within ten years. Failing to act in time can permanently block your right to recover damages.

If the other driver’s insurance company unreasonably delays or denies your claim, it may be acting in bad faith. Under 215 ILCS 5/154.6, improper claims practices include failing to communicate, not conducting a prompt investigation, or offering unfair settlements. Keep detailed documentation of all correspondence, claim submissions, and responses. Victims of bad faith may be entitled to damages beyond the original claim, including legal services. A lawyer can help pursue penalties and hold the insurer accountable.

While you can file a car insurance claim on your own, many situations call for legal representation. If you’ve suffered a severe injury, are facing denied claims, or are dealing with low insurance limits, an attorney can help you recover damages. Legal help is especially important in UM/UIM disputes, crashes involving rideshare drivers, or accidents with commercial vehicles. A Chicago traffic accident lawyer can also assist when out-of-state car insurance laws complicate the claims process.