100% Focus on Your Recovery,

Chicago Auto Accident Lawyer

Chicago Auto Accident Lawyer

Our Team of Attorneys Are Committed to Maximizing the Value of Your Case

Can you have out-of-state car insurance? It’s a common question, especially for people living between states, traveling for school or work, or relocating temporarily. At our law firm, we’ve seen how easily insurance coverage issues can complicate an auto accident claim, especially when policies don’t match up with where the driver lives or where the accident happened.

Our Chicago auto accident attorneys help clients sort through confusing coverage questions, identify insurance problems before they become legal obstacles, and hold insurance companies accountable when they deny valid claims.

Whether you’re a student attending college in a new state, a military member stationed outside Illinois, or simply splitting time between two homes, it’s essential to understand how your auto insurance policy works and when it might be putting you at risk.

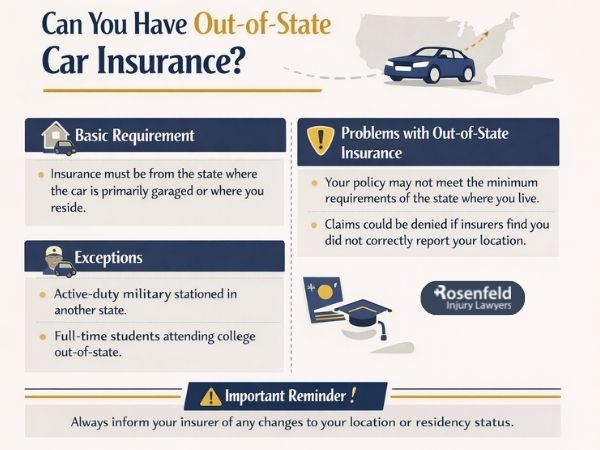

Car insurance rules are based on where your vehicle is kept most of the time, not necessarily where you used to live, where your mail goes, or where you’d prefer to insure it. If you’ve moved to a new state, even temporarily, your auto insurance company will generally require you to update your insurance policy to reflect the new primary residence and vehicle registration location.

Most states require drivers to insure a car in the same state where it is “garaged,” meaning where it is regularly parked overnight. For example, if you moved from Indiana to Illinois and now park your car at your Chicago apartment, you’re expected to carry an auto insurance policy issued under Illinois insurance laws, not Indiana’s. Ignoring this can affect your insurance coverage, delay claim approvals, or even result in a claim denial after a crash.

Insuring a vehicle under an address from a different state to avoid higher premiums or stricter minimum coverage requirements could also create problems with your insurance provider. Each auto insurance company has its own rules, but most expect accurate, up-to-date information reflecting where the car is located and where the driver lives.

There are some situations where keeping an out-of-state auto insurance policy may be acceptable. For example, college students often keep a vehicle insured under their parents’ insurance policy even if they’re attending school in a new state. This is usually allowed as long as the student is still considered a dependent, doesn’t establish a permanent residence, and the car is registered under the family’s name and address.

Military personnel may also qualify for exceptions. If you’re military stationed away from your primary residence, you may be allowed to continue using your American car insurance policy from your home state while living elsewhere. This typically applies as long as your vehicle registration and driver’s license are valid and linked to your home of record.

Temporary job assignments, extended road trips, or short-term stays in another state usually don’t require a new car insurance policy, provided your legal residence hasn’t changed. However, if you take a new job, rent long-term housing, or spend most of the year in a different state, your current carrier might require you to adjust your insurance coverage or open a separate insurance policy.

Falsifying information on a car insurance policy can lead to serious consequences, both from your insurance company and from law enforcement. One common type of insurance fraud is “rating fraud,” which happens when someone provides a false address to get cheaper rates or meet less demanding minimum coverage car insurance standards.

This includes:

These actions can cause your insurance provider to deny claims, cancel your policy, or even report you for fraud. Some states treat this as a misdemeanor or felony offense, especially if you provided false documentation or knowingly misrepresented your situation.

Each state law varies, but in most states, the penalties may include hefty fines, criminal charges, a revoked driver’s license, and civil liability if you cause a crash and your insurance is declared invalid.

Under the Illinois Vehicle Code (625 ILCS 5/7-601), all drivers are required to maintain a minimum level of auto insurance to operate a vehicle legally. This law applies whether the vehicle is owned, leased, or borrowed. The required minimum coverage car insurance in Illinois includes:

Drivers must also carry uninsured motorist coverage at the same bodily injury limits. Your car insurance policy must remain active at all times while the vehicle is registered in the state. Failing to show proof of insurance coverage can result in fines, license suspension, and vehicle registration penalties.

If you’re living in Illinois but using out-of-state auto insurance, your insurance company may not meet these requirements, putting you at risk of being underinsured or non-compliant with state regulations.

Yes, most car insurance policies issued in Illinois include nationwide coverage, meaning you’re typically covered when driving in any of the multiple states within the U.S. If you’re temporarily in a new state and get into an accident, your insurance company will usually adjust your liability limits to meet that state’s minimum coverage requirements. This is commonly referred to as a “broadening clause.”

For example, if you’re insured in Illinois and drive through Georgia, where higher liability limits are required, your auto insurance policy may automatically raise your limits to stay compliant. However, this adjustment only applies if your policy is active and your vehicle is being used legally.

There are exceptions. Standard insurance coverage usually does not apply in Mexico unless you’ve added a specific rider. It also won’t cover non-permissive use–such as if someone takes your car without your permission–or commercial use like rideshare driving, unless you have proper endorsements.

Rental cars can also create confusion. Your personal car insurance policy may extend to rentals within the U.S., but you should check with your insurance provider. The same applies to using a vehicle for work; without a commercial insurance policy, you may not be fully covered.

Always confirm with your insurance agent before taking a road trip, renting a car, or working as a rideshare driver.

If you borrow a car while you’re in a new state, auto insurance is generally vehicle-based, meaning it follows the vehicle, not the driver. This means the car insurance policy belonging to the vehicle’s owner is considered primary. If there’s an accident, their insurance coverage is typically used first to pay for damages or injuries. If the costs exceed the owner’s policy limits, your own car insurance (if you have one) may serve as secondary coverage.

However, this only works if you’re driving with permission and you’re not an excluded driver on the owner’s policy. Some insurance policies specifically name people who are not covered, even if they borrow the vehicle. If you’re part of the owner’s household but not listed on their policy, there could also be coverage issues, especially if the insurance company believes you’re trying to avoid paying for a separate car insurance policy.

Driving a friend’s or family member’s car in another state may also raise questions if you’re staying in that state year-round. If you’re living there full-time, the insurer might require you to be added to the policy or get a separate policy. Always check with the insurance agent or current insurer to make sure you’re properly covered.

If you rent a car in another state, your personal car insurance policy usually applies, but don’t limit yourself to assuming all coverage gaps are handled. Most personal auto insurance policies provide nationwide coverage, which means liability and sometimes collision or comprehensive coverage will follow you when driving a rental vehicle. However, the details depend on your specific insurance provider and the type of policy you have.

Your liability insurance will often extend to a rental, meeting the legal minimum coverage requirements in the same state where the rental takes place. That said, the auto insurance company only pays up to the limits listed in your policy. If you’re involved in a crash and don’t carry collision or comprehensive coverage, you may be responsible for damage to the rental unless you’ve bought a collision damage waiver from the rental company.

Rental car accident coverage from the rental company often includes a supplemental insurance option, which can cover liability beyond your personal policy limits or add protection for medical expenses and theft. While rental companies must provide some liability coverage, it’s usually the bare legal minimum and may not offer much real protection.

To avoid surprises, contact your insurance agent before renting. If your current carrier doesn’t offer adequate coverage, consider buying a standalone policy for the rental period.

If you’re involved in a crash and either you or the other driver has an out-of-state car insurance policy, the claims process will still move forward, but several factors can complicate things. First, car insurance companies will evaluate the claim based on the state where the accident occurred, not where the policy was issued. That means Illinois’ fault rules apply, since it’s an at-fault state. The insurer will determine liability and process claims accordingly.

When a policy is written in another state, insurers usually adjust the coverage to meet Illinois’s minimum coverage requirements, including liability limits and uninsured/underinsured motorist (UM/UIM) protections. UM/UIM often follow the driver, not the vehicle, so it may still apply if you’re hit by someone with little or no insurance.

However, if the insurance policy is out of compliance – such as failing to meet Illinois’s required limits or lacking insurance cover altogether – the insurer might limit payouts or deny the claim. In some cases, you may need to file a claim against your own auto insurance policy for coverage.

Issues involving out-of-state auto insurance can get complicated fast, especially if you’re facing a denied claim, a residency dispute, or penalties tied to vehicle registration. You may need legal help if your insurance company claims you failed to update your primary residence, questions where your vehicle is garaged, or accuses you of providing false information to lower your premiums.

Disagreements over liability, minimum coverage car insurance limits, or how insurance laws apply across multiple states are also strong reasons to speak with an attorney. These disputes often arise after an accident, especially when drivers hold policies from different states with different rules.

Our Chicago traffic accident attorneys help clients sort through these conflicts and protect their right to compensation. If you’re unsure whether your insurance coverage still applies or you’re facing penalties related to a car insurance policy, don’t wait to get answers.