100% Focus on Your Recovery,

Chicago Auto Accident Lawyer

Chicago Auto Accident Lawyer

Our Team of Attorneys Are Committed to Maximizing the Value of Your Case

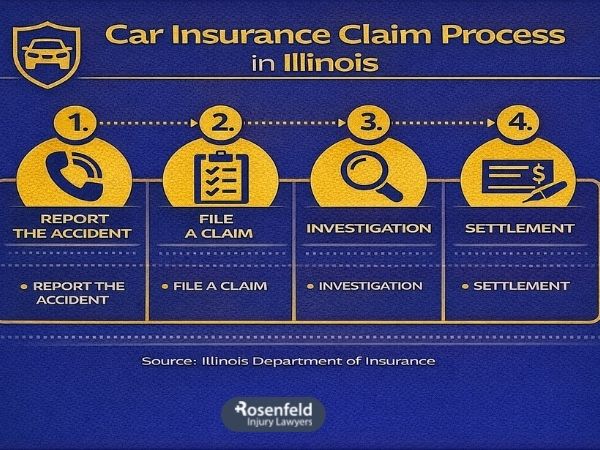

When someone comes to our Chicago-based firm after a serious car accident, one of the first things we help them understand is the car insurance claim process in Illinois. Even a routine fender-bender can feel overwhelming when you’re suddenly dealing with an insurance company, medical bills, a damaged car, and confusing insurance contracts. From the moment you reach out, we stand with you and guide you through every step so youn can move forward with clarity and confidence.

The first step in the claim process is making sure the crash is properly reported. Illinois law sets clear requirements, and following them helps strengthen your compensation claim and prevents disputes later.

Under 625 ILCS 5/11-407, drivers must contact law enforcement after any accident that results in injury, death, or significant property damage. In Chicago, this typically means calling CPD to the accident scene.

An official incident report documents involved parties, roadway conditions, witness statements, visible damage, and whether any citations were issued. Insurance companies rely heavily on this report when determining fault and liability.

We always encourage our clients to request the report number before leaving the scene. This one step can make the rest of the claim smoother.

Illinois law also requires drivers to exchange basic contact and insurance information, including:

Collecting accurate details from the other driver helps avoid coverage disputes and ensures that both drivers’ insurance companies can properly determine who is responsible.

Under 215 ILCS 5/143.1, you must also notify your insurance company “within a reasonable time.” Most insurance companies interpret this very strictly, sometimes requiring same-day or next-day notice.

Your initial report should include:

We routinely help clients make this call so they avoid mistakes or statements that could later be used to dispute liability.

Before leaving the scene, if you are medically able, document as much relevant information as possible, including:

This evidence helps prevent liability disputes and protects you if the insurance company later claims the repair expenses or injuries were not related.

In Illinois, you may file your insurance case through:

If another negligent driver caused the crash, their liability insurance pays for your property damage, medical expenses, and other losses, up to their policy limits. This process generally requires:

You may file through your own insurance company when:

These options can help you move forward faster. In most cases, your insurance company handles reimbursement from the other party later.

Each path has its own requirements, and we help clients choose the route that protects their claims and speeds the process.

Once a claim is opened, the insurance adjuster becomes the main point of contact. This person gathers facts, evaluates liability, and estimates costs.

Here’s what the adjuster typically reviews:

The adjuster examines the car for:

They may request photos, inspect the car at a vehicle repair facility, or send you to a drive-in assessment location.

The adjuster evaluates:

This determination affects whether the claim is paid, reduced, or denied.

For injury claims, the adjuster reviews:

Their assessment heavily influences the settlement value.

Adjusters do not represent your interests, they represent the insurance company. We stand with you throughout this stage to ensure your rights are protected and the adjuster receives only what is necessary.

Once coverage is accepted, the vehicle restoration portion of the claim process begins.

You can usually obtain estimates from any certified repair center. Many insurance companies also have preferred shops, but you are not required to use them.

A typical process includes:

Most insurance policies allow you to choose your own repair shop, though insurance companies may encourage certain partners. You have the right to select who works on your vehicle.

A total loss means repairs exceed a certain percentage of the car’s value. In that case:

You may be responsible for storage fees at a storage facility if the vehicle stays there too long. We help clients navigate those deadlines so costs don’t escalate.

Once liability and damages are confirmed, the insurance company issues payment according to the type of insurance purchased.

In most situations, payments come in separate checks: one for property damage, one for injuries.

It covers:

This pays for injuries caused by the driver who caused the crash, including:

Depending on your car insurance plan, your payout may include:

Even straightforward crashes can become complicated. Some of the most common issues we see include:

For example, insurance companies may claim:

Delays often arise from:

Denials may result from:

Insurance companies may undervalue:

Adjusters may downplay:

We guide clients through these challenges so they feel supported and never pressured into accepting an unfair offer.

A denial doesn’t mean the end of your case. You still have options, and we stand with you through each one.

Ask the insurance company to detail:

This may include:

Most insurance companies have multi-step review procedures. We help clients pursue these appeals and prepare the strongest record possible.

If you face serious injuries, substantial property damage, or a complex dispute, involving a Chicago car accident lawyer can protect your rights and ensure no release or document is signed prematurely. Many clients come to us after trying to handle these matters alone, and once we step in, the process becomes far more manageable.

As a Chicago traffic accident lawyer team, we help our clients at every stage of the journey, from the moment the accident happens to the final payout.

Here’s how we support you:

We handle car accident cases on a contingency fee basis, meaning you owe no upfront costs and no attorney fees unless we recover compensation for you. Your consultation is always free, and we’re here to help you understand your rights, your options, and every step of the Illinois car insurance case process.

Whenever you’re ready, contact us. We stand with you, and we believe in your case.