100% Focus on Your Recovery,

Chicago Auto Accident Lawyer

Chicago Auto Accident Lawyer

Our Team of Attorneys Are Committed to Maximizing the Value of Your Case

When someone comes to our Chicago-based firm after a Lyft accident on the Kennedy, on Lake Shore Drive, or on a neighborhood street in Logan Square or Hyde Park, one of the first issues we walk through together is how Lyft insurance requirements work in Illinois. Many of our clients feel overwhelmed by medical bills, lost income, and uncertainty about which insurance provider has to pay.

We stand with you from day one. As Chicago Lyft accident attorneys, our role is to help you understand your legal options, the available insurance coverage, and the steps you can take to protect yourself under Illinois law.

Lyft, like other rideshare companies, operates under a specific regulatory framework in Illinois that determines what insurance applies at each stage of a Lyft ride. Knowing how these coverage periods work can make a life-changing difference for injured passengers, drivers, and anyone else involved in a crash.

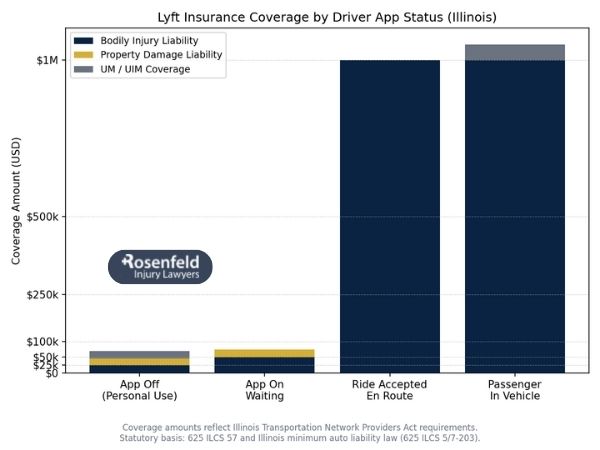

Yes, under the Illinois Transportation Network Provider Act (625 ILCS 57/), Lyft must provide liability coverage when a driver is using the Lyft app for commercial activity. Illinois classifies Lyft drivers as Transportation Network Providers (TNPs), meaning they are not taxi drivers or commercial livery operators; instead, their insurance coverage depends entirely on their app status at the moment of the accident.

In other words, Lyft insurance coverage is not constant. It only applies when the driver is:

Lyft’s coverage structure mirrors the tiers required for rideshare platforms under Illinois law. These rules are similar to Uber’s insurance framework but operate independently through Lyft’s insurance provider.

Lyft publicly outlines its policies at its official website. We rely on this official source when evaluating a Lyft insurance policy, filing Lyft insurance claims, or addressing disputes between insurers. Lyft’s page also clarifies when contingent collision coverage, comprehensive coverage, and personal auto insurance policy exclusions apply.

We will outline this information throughout the sections below.

When a Lyft driver is fully offline, meaning the app is closed and the driver is not available for ride requests, Lyft provides no insurance coverage whatsoever. Illinois law treats this as ordinary personal driving, and only the driver’s personal auto insurance policy applies.

However, many personal policies contain express commercial insurance exclusions. That means they may refuse to cover accidents caused while the driver was:

If the insurer believes the driver was engaged in any type of commercial use, they may deny coverage, which creates complications for anyone injured in the accident.

Because of these risks, we regularly help clients navigate disputes between Lyft’s insurer and the driver’s insurance company about whether the app was actually on or off at the moment of impact. These disputes can determine whether there is access to liability insurance, personal injury protection, medical payments, or collision protection.

This stage is known as “Period 1.” The Lyft driver is logged into the app and available for trips but has not yet accepted a ride request.

Illinois requires reduced liability insurance during this period, and Lyft follows the state’s minimum structure:

This is basic coverage only. It is not enough to fully compensate many victims who suffer serious injuries, especially in high-speed crashes.

If a Lyft accident occurs during Period 1:

Because Period 1 has lower available coverage, disputes over fault, coverage triggers, and the driver’s app status are common. We frequently step in when two insurance providers argue about who must pay.

Once the Lyft driver accepts a request and is driving to pick up a passenger, “Period 2” begins. During this stage, Illinois law and Lyft’s policies provide much higher policy limits, reflecting the increased risk to the public.

Period 2 coverage includes:

This is when Lyft’s policy becomes primary, meaning the victim does not have to exhaust the rideshare driver’s personal policy first.

If someone is hurt while the driver is on the way to a pickup, such as a driver of another car, pedestrian, cyclist, or anyone in other vehicles:

We help our clients document fault, evaluate available sources of coverage, and challenge any attempt by insurers to avoid paying fair compensation.

This is “Period 3,” the highest form of insurance coverage under Illinois law and the Transportation Network Provider Act. During an active ride, when a passenger is in the vehicle, Lyft must provide:

If you are a passenger during a Lyft ride and an accident occurs, Lyft’s $1M policy is designed to step in immediately. You may be entitled to compensation for:

We guide clients through this process and help them hold the responsible insurance companies accountable.

When you pursue a Lyft accident claim, the claims process can feel overwhelming. Many clients come to us after dealing with multiple insurers who each try to place blame on someone else. We stand with you throughout this process and help you understand how to move forward with clarity.

You must notify Lyft through the app or website as soon as possible. Lyft will route the claim to its insurer.

Depending on the driver’s app status, you may need to file with:

Strong supporting evidence may include:

Insurers look at:

Multiple insurers may argue about fault, policy limits, or who must pay first. We help our clients push back against unfair denials and seek maximum compensation.

Because Lyft’s policy changes depending on whether the driver was:

Insurers often dispute which insurance policy applies. These disputes affect access to full compensation for serious injuries, lost income, or long-term medical care.

Our firm routinely investigates app data, phone logs, digital timestamps, and location history to confirm the driver’s status at the exact moment of the crash.

If you were injured in a Lyft crash, you don’t have to navigate this process alone. As Chicago traffic accident attorneys, we help clients understand their legal options, protect their rights, and pursue the compensation they deserve after rideshare collisions. We believe in your case, and we stand with you every step of the way.

Our experienced attorney team helps with:

We handle these matters on a contingency fee basis, meaning you owe no upfront costs and no attorney fees unless we recover compensation for you.

If you or a loved one has been involved in a Lyft accident anywhere in Chicago or Cook County, contact us for a free consultation. We’re here to help you rebuild, protect your rights, and move forward with clarity and support.